Why Power Is the Bottleneck for AI

The next wave of AI capex is no longer constrained by demand for GPUs alone. Grid capacity, transformers, switchgear, turbines, and cooling are increasingly the hard limit.

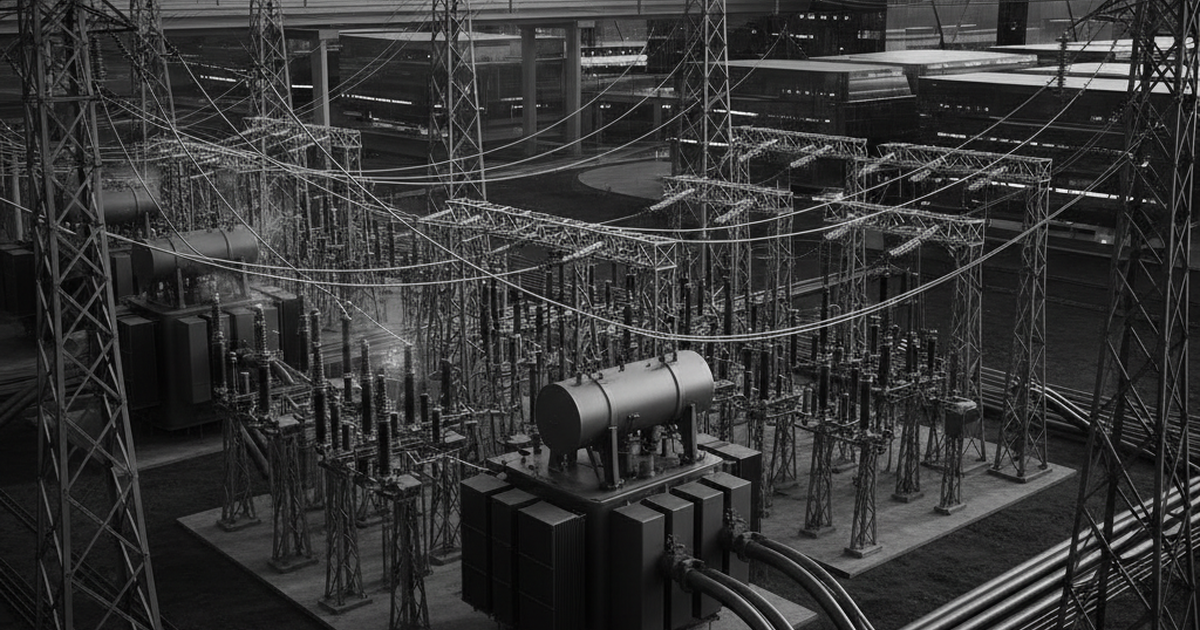

The market still talks about AI as if the key variable is compute demand. That is only half the picture. The deeper issue is whether the physical grid can actually support the scale of deployment hyperscalers are now underwriting.

A modern AI facility is not a normal data center. Rack densities are rising sharply, liquid cooling is becoming mandatory, and the amount of supporting electrical infrastructure per megawatt of IT load is increasing. That means the winners are not just chip suppliers. They are also the companies touching transformers, switchgear, backup power, grid equipment, cooling systems, and generation capacity.

The constraint is moving downstream

In the first leg of the cycle, investors focused on GPU scarcity. In the next leg, the market has to underwrite the supporting infrastructure required to actually energize those clusters. That shifts attention toward:

- GE Vernova for generation exposure and grid modernization

- Vertiv for thermal management and power distribution

- Eaton for electrical equipment and switchgear

- Utilities and power producers where load growth becomes visible in contract structures

Why this matters now

Lead times across key electrical components remain long. Permitting for generation and transmission projects is slow. Utilities are increasingly prioritizing large industrial loads, but that doesn’t mean capacity appears overnight. The mismatch between AI demand curves and physical deployment timelines creates a durable bottleneck.

That bottleneck matters for investors because it extends the duration of the capex cycle. It also broadens the opportunity set beyond semiconductors.

What we’re watching

We care less about splashy model demos than we do about signals like:

- accelerated utility interconnection queues,

- comments around transformer and switchgear lead times,

- power usage effectiveness trends,

- hyperscaler capex guidance tied to regional buildouts.

The market is still underpricing how physical this AI buildout really is. Power is no longer a side constraint. It is becoming the gating factor.